August 12, 2020

Arbitrability of the disputes/differences Insurance Policy

If the insurance co. disputes or repudiates the claim or the insured voluntarily executes the discharge voucher in accord and satisfaction of the claim, then there cannot be any reference of any dispute to arbitration…

Contracts of insurance are in the nature of contract of indemnity and it entitles the insured for the reimbursement of actual loss in terms of the insured perils and policy condition. The Insurance Act, 1938 and Insurance Regulatory and Development Authority (Protection of Policyholders’ Interests) Regulations, 2002 prescribe guidelines for settling of claim by the insurance co. Section 64 UM (2) of the Insurance Act, 1938 mandates that no claim in respect of a loss equal to or exceeding twenty thousand rupees in value on any policy of insurance be admitted for payment, unless the insurer obtains a report on the loss that has occurred from a person who holds a license issued under sub-section (1) of Section 64-UM of the Act as a ‘surveyor’ or ‘loss assessor’. The proviso to sub-section (2) however, retains the right of the insurance co. to settle a claim for an amount different from that assessed by the surveyor. This proviso further permits the insurance co. to obtain a second or further report where considered appropriate or expedient in the circumstances of a case, based upon which the claim could be settled for a different amount than as assessed earlier. Regulation 9 (5) of IRDA (Protection of Policyholders’ Interests) Regulation, 2002 provided that on receipt of the survey report, the insurance co. shall settle the claim within 30 days from the receipt of the report and if or any reason claim is not maintainable, the reason for the same be also communicated within 30 days.

Relevant Provisions:

“Section 64UM Licensing of Surveyors and Loss Assessors

(2) No claim in respect of a loss which has occurred in India and requiring to be paid or settled in India equal to or exceeding twenty thousand rupees in value on any policy of insurance, arising or intimated to an insurer at any time after the expiry of a period of one year from the commencement of the Insurance (Amendment) Act, 1968, shall, unless otherwise directed by the 8 [Authority], be admitted for payment or settled by the insurer unless he has obtained a report, on the loss that has occurred, from a person who holds a license issued under this section to act as a surveyor or loss assessor (hereafter referred to as “approved surveyor or loss assessor”): Provided that nothing in this sub section shall be deemed to take away or abridge the right of the insurer to pay or settle any claim at any amount different from the amount assessed by the approved surveyor or loss assessor.

Reg.9 Claim Procedure in respect of general insurance policy:

(5) On receipt of the survey report or the additional survey report, as the case may be, an insurer shall within a period of 30 days offer a settlement of the claim to the insured. If the insurer, for any reasons to be recorded in writing and communicated to the insured, decides to reject a claim under the policy, it shall do so within a period of 30 days from the receipt of the survey report or the additional survey report, as the case may be.”

Arbitration Clause in the insurance policy:

“If any dispute or difference shall arise as to the quantum to be paid under this policy (liability being otherwise admitted) such difference shall independently of all questions be referred to the decision of a sole arbitrator to be appointed in writing by the parties to or if they cannot agree upon a single arbitrator within 30 days of any party invoking arbitration, the same shall be referred to a panel of three arbitrators, comprising two arbitrators, one to be appointed by each of the parties to the dispute/difference and the third arbitrator to be appointed by such two arbitrators and arbitration shall be conducted under and in accordance with the provisions of the Arbitration and Conciliation Act, 1996.

It is clearly agreed and understood that no difference or dispute shall be referable to arbitration as hereinbefore provided, if the Company has disputed or not accepted liability under or in respect of this policy.

………..”

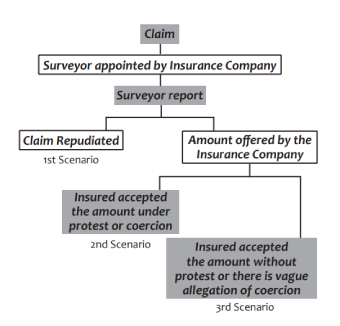

Now the question arises whether all the disputes or differences under the insurance policy are arbitrable –

First Scenario

When we carefully examine the aforesaid arbitration clause, it is quite clear that once the insurance co. disputes the liability under or in respect of the policy, there can be no reference to arbitration. There is no stipulation in the policy that once the liability is disputed, such a controversy to be referred to arbitration. The amount to be paid, has been distinguished from the liability to pay anything, no action can be commenced until the insurance co. shall have determined such amount. It is quitelimpid that once the insurance co. disputes the liability under the policy and repudiates the same or closes the same as no – claim, there can be no reference to the arbitrator. The principle of un-conscionability of the terms & conditions of the policy and/or lack of bargaining power does apply in case of interpretation of arbitration clause in the policy. In the case of General Assurance Society Ltd. Vs. Chandumull Jain – AIR 1996 SC 1644, Oriental Insurance Co. Ltd. Vs. Samayanallur Primary Agricultural Coop Bank – AIR 2000 SC 10 and United India Insurance Co. Ltd. Vs. Harchand Rai Chandan Lal – (2004) 8 SCC 644, the Hon’ble Supreme Court in no uncertain terms has held that the parties are bound by the clauses enumerated in the policy and the court does not transplant any equity to the same by rewriting a clause.

In the case of Oriental Insurance Company Limited Vs. Narbheram Power and Steel Pvt. Ltd. – (2018) 6 SCC 534, the Hon’ble Supreme Court held that the second part of the arbitration clause clearly spells out that the parties have agreed and understood that no differences and disputes shall be referable to arbitration if the insurance co. has disputed or not accepted the liability. If the insurance co. has, on facts, repudiated the claim by denying accepting the liability, no inference can be drawn that there is some kind of dispute with regard to quantification. It is a denial to indemnify the loss and such a situation falls on all fours within the concept of denial of disputes and non-acceptance of liability. It is not one of the arbitration clauses which can be interpreted in a way that denial of a claim would itself amount to dispute and, therefore, it has to be referred to arbitration. The parties are bound by the terms and conditions agreed under the policy and the arbitration clause contained in it. The language used in the second part is absolutely categorical and unequivocal inasmuch as it stipulates that it is clearly agreed and understood that no difference or disputes shall be referable to arbitration if the insurance co. has disputed or not accepted the liability. Therefore, the only remedy which the insured can take recourse to is to institute a civil suit for ventilation of the grievances.

Second Scenario

Where insured issues a full and final discharge voucher confirming that he has received the payment in full and final satisfaction of all claims, and he has no outstanding claim, that amounts to discharge of the contract by acceptance of performance and the party issuing the discharge voucher cannot thereafter make any fresh claim or revive any settled claim. Nor can he seek reference to arbitration in respect of any claim. However, if the insured who has executed the discharge voucher, alleges that the execution of such discharge voucher was on account of fraud/coercion/undue influence practiced by the insurance co. and is able to establish the same, then obviously the discharge of the contract by such agreement/voucher is rendered void and cannot be acted upon and any dispute raised by the insured would be arbitrable.

The Hon’ble Supreme Court in National Insurance co. Ltd. vs. Boghara Polyfab Pvt. Ltd – (2009) 1 SCC 267 examined the right of the insured to invoke the remedy of arbitration after execution of discharge voucher, resistance of reference by the insurance co. to arbitration on the ground that the insured has issued a full and final settlement discharge voucher and the insured content that he was constrained to issue it due to coercion, undue influence and economic compulsion. The Hon’ble Supreme Court after examining law laid down in Union of India Vs. Kishorilal Gupta – (1960)1 SCR 493, Naithani Jute Mills Ltd Vs. Khyaliram Jagannath – (1968) 1SCR821, Damodar Valley Corporation Vs. K.K. Kar – (1974) 2SCR240, United India Insurance Co. Ltd Vs. Ajmer Singh Cotton & General Mills – AIR1999 SC 3027, National Insurance Co. Ltd Vs. Nipha Exports (P) Ltd – (2006) 8 SCC156, National Insurance Co. Ltd Vs. Sehtia Shoes – (2008) 5 SCC400 and Central Inland Water Transport Corporation Ltd Vs. Brojo Nath Ganguly – (1986) II LLJ 171 SC, nicely culled out certain illustrations as to when claims are arbitrable and when they are not, when discharge of contract by accord and satisfaction are disputed by the insured:-

(i) A claim is referred to conciliation or a pre-litigation Lok Adalat. The parties negotiate and arrive at a settlement. The terms of settlement are drawn up and signed by both the parties and attested by the Conciliator or the members of the Lok Adalat. After settlement by way of accord and satisfaction, there can be no reference to arbitration.

(ii) A claimant makes several claims. The admitted or undisputed claims are paid. Thereafter, negotiations are held for settlement of the disputed claims resulting in an agreement in writing settling all the pending claims and disputes. On such settlement, the amount agreed is paid and the contractor also issues a discharge voucher/no claim certificate/full and final receipt. After the contract is discharged by such accord and satisfaction, neither the contract nor any dispute survives for consideration. There cannot be any reference of any dispute to arbitration thereafter.

(iii) A contractor executes the work and claims payment of say Rupees Ten Lakhs as due in terms of the contract. The employer admits the claim only for Rupees six lakhs and informs the contractor either in writing or orally that unless the contractor gives a discharge voucher in the prescribed format acknowledging receipt of Rupees Six Lakhs in full and final satisfaction of the contract, payment of the admitted amount will not be released. The contractor who is hard-pressed for funds and keen to get the admitted amount released, signs on the dotted line either in a printed form or otherwise, stating that the amount is received in full and final settlement. In such a case, the discharge is under economic duress on account of coercion employed by the employer. Obviously, the discharge voucher cannot be considered to be voluntary or as having resulted in discharge of the contract by accord and satisfaction. It will not be a bar to arbitration.

(iv) An insured makes a claim for loss suffered. The claim is neither admitted nor rejected. But the insured is informed during discussions that unless the claimant gives a full and final voucher for a specified amount (far lesser than the amount claimed by the insured), the entire claim will be rejected. Being in financial difficulties, the claimant agrees to the demand and issues an undated discharge voucher in full and final settlement. Only a few days thereafter, the admitted amount mentioned in the voucher is paid. The accord and satisfaction in such a case is not voluntary but under duress, compulsion and coercion. The coercion is subtle, but very much real. The ‘accord’ is not by free consent. The arbitration agreement can thus be invoked to refer the disputes to arbitration.

(v) A claimant makes a claim for a huge sum, by way of damages. The respondent disputes the claim. The claimant who is keen to have a settlement and avoid litigation, voluntarily reduces the claim and requests for settlement. The respondent agrees and settles the claim and obtains a full and final discharge voucher. Here even if the claimant might have agreed for settlement due to financial compulsions and commercial pressure or economic duress, the decision was his free choice. There was no threat, coercion or compulsion by the respondent. Therefore, the accord and satisfaction is binding and valid and there cannot be any subsequent claim or reference to arbitration.”

Thus, the position of law is very clear that a claim for arbitration cannot be rejected merely or solely on the ground that a settlement agreement or discharge voucher had been executed by the insured, if its validity is disputed by the insured and prima facie shows that the accord and satisfaction was not voluntarily but under duress, compulsion and coercion.

Third Scenario

What if the insured voluntarily executed the discharge voucher and received the amount offered by the insurance co. or protest was raised after some time could validly invoke the jurisdiction under Section 11 of the Arbitration and Conciliation Act 1996, was examined by the Hon’ble Supreme Court in the case of New India Assurance Company Ltd. Vs. Genus Power Infrastructure Ltd. – (2015) 2 SCC 424. The Hon’ble Supreme Court after relying upon the proposition of law laid down in the case National Insurance Co. Ltd. v. Boghara Polyfab Pvt. Ltd. (supra) and Union of India v. Master Construction Co. – (2011) 12 SCC 349 held that the Chief Justice/his designate exercising jurisdiction under Section 11 of the Act will consider whether there was really accord and satisfaction or discharge of contract by performance. The Hon’ble Court further held that it may not be proper to burden a party, who contends that the dispute is not arbitrable on account of discharge of contract, with huge cost of arbitration merely because plea of fraud, coercion, duress or undue influence has been taken by the insured. A bald plea of fraud, coercion, duress or undue influence is not enough and the party who sets up such a plea must prima facie establish the same by placing material before the Chief Justice/his designate. If the Chief Justice/his designate finds some merit in the allegation of fraud, coercion, duress or undue influence, he may decide the same or leave it to be decided by the arbitrator. On the other hand, if such a plea is found to be an afterthought, make-believe or lacking in credibility, the matter must be set at rest then and there.

In the case of United India Insurance Co. Ltd. Vs. Antique Art Exports Pvt. Ltd. – (2019) 5 SCC 362, the Hon’ble Supreme re-affirmed the aforesaid law and held that mere plea of fraud, coercion or undue influence in itself is not enough and the party who alleged is under obligation to prima facie establish the same by placing satisfactory material on record before the Chief Justice or his designate to exercise power under Section 11(6) of the Act. In the aforesaid case, the Hon’ble Court rejected the contention of the insured that after insertion of Sub-Section (6A) to Section 11 of the Amendment Act, 2015, the jurisdiction of the Court is denuded and limited mandate of the Court is only to examine the existence of the arbitration agreement and held that it is always necessary to ensure that the dispute resolution process does not become unnecessarily protracted.

It is thus clear that if the insurance co. disputes or repudiates the claim or the insured voluntarily executes the discharge voucher in accord and satisfaction of the claim, then there cannot be any reference of any dispute to arbitration.

Disclaimer – The views expressed in this article are the personal views of the author and are purely informative in nature.